Company Update | Banking

December 1, 2016

Federal Bank

BUY

CMP

`71

Target Price

`85

Loan growth to remain decent, albeit lower pace seen in the last two quarters: In

Investment Period

12 Months

Q1FY17, the bank reported 19% loan growth, which further accelerated to 27%

in Q2FY17, backed by 47% jump in corporate loan book. Retail loans also were

Stock Info

strong. Gold loan, which had been under pressure and also saw degrowth in

previous quarters, saw a comeback thus contributing to the growth. While the

Sector

Banking

process of demonetization is likely to have an impact and loan growth might

Market Cap (` cr)

12,156

slow down in Q3 & Q4FY17, we expect Federal Bank to bounce back to 17-18%

Beta

1.3

YoY loan growth trajectory in FY18.

52 Week High / Low

86 / 41

Deposit growth will get a further boost, CASA to remain high: Deposit growth for

Avg. Daily Volume

515,000

the banking industry witnessed some improvement in Q2FY17. Federal bank

reported a jump of 17% in deposit base on top of 12.5% growth in Q1FY17. We

Face Value (`)

2

have already seen rush in bank deposits amid the demonetization move, this will

BSE Sensex

25,850

further accelerate the growth in deposit base. Though interest rates will further

Nifty

7,976

come down, the banking industry including Federal Bank will continue to see

surge in deposits in the months to come.

Reuters Code

FED.BO

Asset quality stress has started stabilizing: High slippages and resultant credit

Bloomberg Code

FB@IN

cost had dented the profitability of Federal Bank in FY16. However in the last two

quarters, the slippages have been under control. Q2FY17 slippages of

`266cr

was the lowest in the last five quarters. Total stressed asset at

4.8%

Shareholding Pattern (%)

(NNPAs1.61% + Restructured 3.2%) is not alarming. While it’s too early to say

Promoters

0.0

that the trouble is over, the initial signs are encouraging. Further quantifying the

impact of demonetization is a challenging task, but it is a fact that SMEs do have

MF/ Banks / Indian Fis

32.8

large cash transactions either for input or for finished goods. While there could

FII/ NRI/ OCBs

43.7

be some incremental pressure on asset quality in the near term, the relatively

improving corporate loan book of Federal Bank gives us comfort.

Indian Public / Others

23.5

High credit cost dented the return ratios so far, expect RoE to bounce back in

FY18: Higher slippages dented the RoE both due to reversal of interest and rise

Abs. (%)

3 m

1 yr

3 yr

in provisions. However, the lower slippages expected in the coming years would

normalize the return ratios and we expect RoE to scale back to 10% trajectory by

Sensex

(6.9)

0.9

26.4

FY18. Further, accelerated loan growth should also support higher fees income

Federal Bank

1.2

19.3

74.4

and consequently RoE.

Outlook and valuation: Federal Bank has already recognized large part of the

3-year price chart

troubled assets as NPAs. While there could be incrementally some degree of

90

stress on the SME book, we believe gradually there should be overall

80

70

improvement in the asset quality backed by the corporate loan book. At the

60

CMP, the stock is trading at 1.4x it FY18 Adj BV. We upgrade the stock to BUY

50

with a target price of `85.

40

30

Key financials (Standalone)

20

Y/E March (` cr)

FY2015

FY2016

FY2017E

FY2018E

10

NII

2,380

2,504

2,899

3,292

-

% chg

6.8

5.2

15.8

13.6

Net profit

1,006

476

746

958

% chg

19.9

(52.7)

56.8

28.4

Source: Company, Angel Research

NIM (%)

3.0

2.9

3.0

3.0

EPS (`)

11.7

2.8

4.3

5.6

P/E (x)

6.0

25.3

16.1

12.6

P/ABV (x)

0.8

1.7

1.5

1.4

Siddharth Purohit

RoA (%)

1.3

0.5

0.8

0.9

022 - 3935 7800 Ext: 6828

RoE (%)

13.0

5.9

8.5

10.1

Source: Company, Angel Research; Note: CMP as of November 30, 2016

Please refer to important disclosures at the end of this report

1

Federal Bank | Company Update

Loan growth to remain decent, albeit lower pace seen in

the last two quarters;

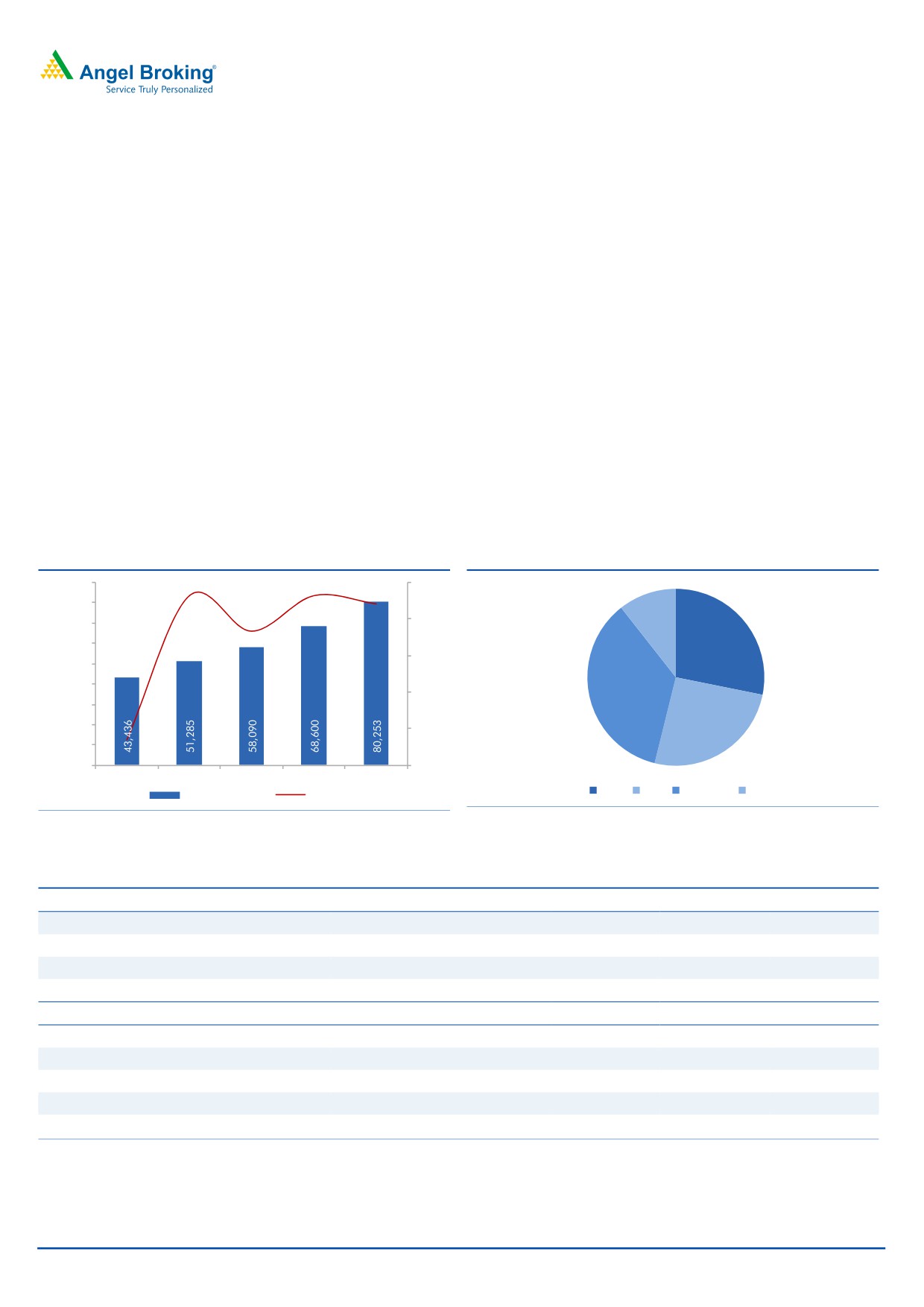

Federal Bank has reported decent loan growth over the last two years. In Q1 and

Q2 of FY17, the bank has seen further acceleration in the loan growth by 19% and

27%, respectively. The phenomenally high growth in Q2FY17 was backed by 47%

jump in loan book from the corporate loan book. Historically, SME has been a

growth driver for Federal Bank and accounts for ~25% of the loan book.

Corporate loans have also been witnessing strong growth in the last few quarters

and now account for 35% of the book compared to 30% in Q1FY16.

While it is difficult to quantify the effect of demonetization on banking space, it is

fair to assume a slowdown in the SME and Corporate segment. The smaller and

micro enterprises depend on cash to large extent both for their input and selling

their final output, and hence there could be a moderation in the loan growth in the

coming two quarters. However, the interest rate regime in India is likely to remain

low for many quarters to come and this should help better credit growth after a

pause that we are likely to see in the next two quarters.

Exhibit 1: Loan Book growth (%)

Exhibit 2: Loan Book Composition (%)

90,000

20.0

18.1

18.1

80,000

17.

0

11

70,000

15.0

13.3

28

60,000

10.0

50,000

40,000

5.0

36

30,000

20,000

-

(1.5)

26

10,000

-

(5.0)

FY14

FY15

FY16

FY17E

FY18E

Retail

SME Corporate

Agri

Advances (` cr)

Growth (%)

Source: Company, Angel Research

Source: Company, Angel Research

Exhibit 3: Loan Composition Trend

Loan Composition (` Cr )

Q1FY16

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Retail

16,035

16,392

14,265

14,987

15,133

17,795

SME

13,011

13,875

14,033

15,172

15,325

16,235

Corporate

15,130

15,272

16,668

19,652

20,693

22,451

Agri

6,159

6,137

6,062

6,636

6,445

6,700

Total

50,335

51,676

51,028

56,447

57,596

63,181

Loan Composition (%)

Retail

31.9

31.7

28.0

26.6

26.3

28.2

SME

25.8

26.8

27.5

26.9

26.6

25.7

Corporate

30.1

29.6

32.7

34.8

35.9

35.5

Agri

12.2

11.9

11.9

11.8

11.2

10.6

Source: Company, Angel Research

December 1, 2016

2

Federal Bank | Company Update

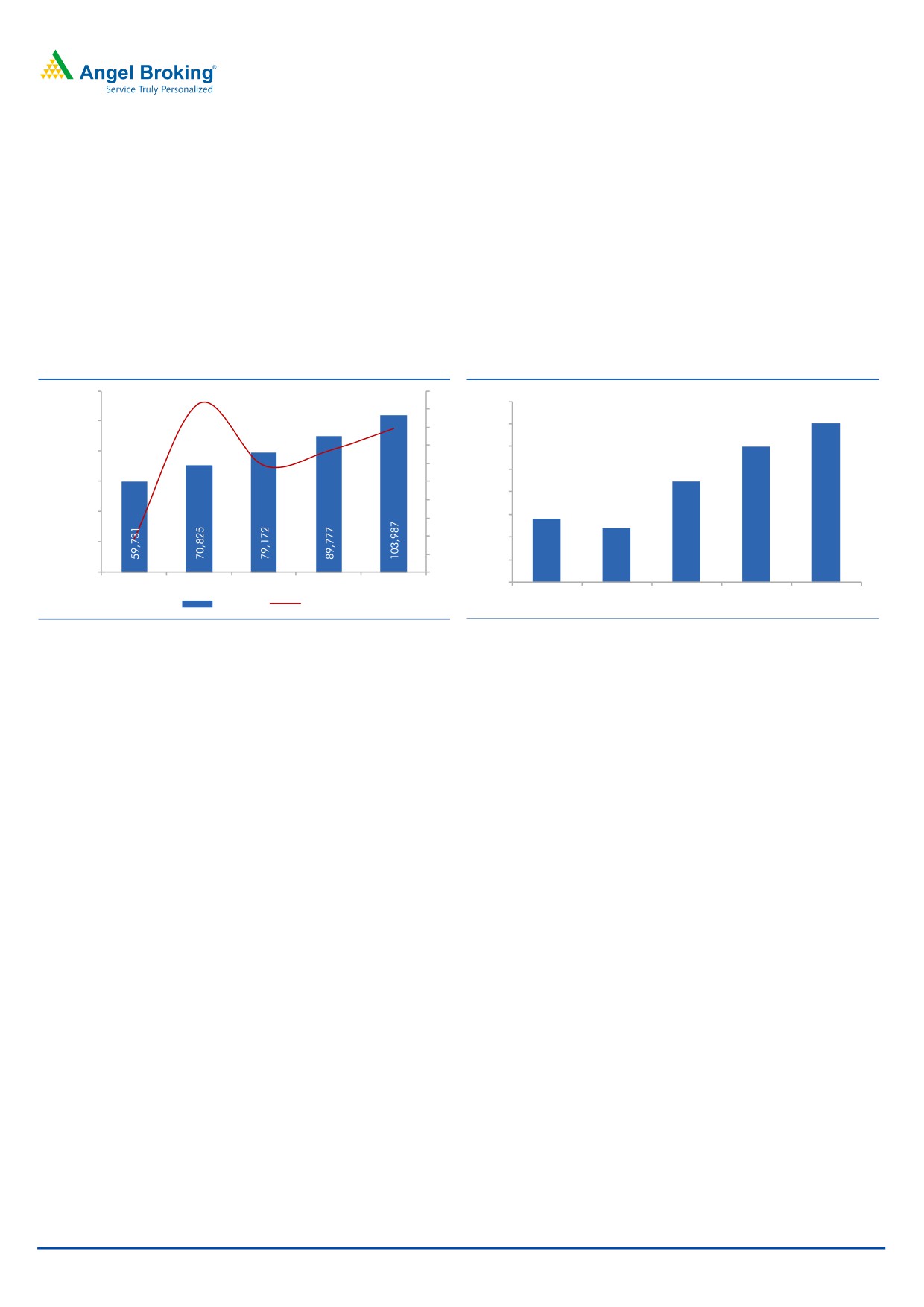

Deposit growth will get a further boost, CASA to remain

high

The deposit growth for the banking industry witnessed some improvement in

Q2FY17. Federal bank reported a jump of 17% in deposit base on top of 12.5%

growth in Q1FY17. We have already seen rush in bank deposits amid the

demonetization move, this will further accelerate the growth in deposit base.

Though interest rates will further come down, the banking industry including

Federal Bank will continue to see surge in deposits in the months to come.

Exhibit 4: Deposit growth trend (` Cr)

Exhibit 5: CASA Ratio (%)

120,000

20

18.6

36.0

18

35.0

100,000

35.0

15.8

16

34.0

14

34.0

80,000

13.4

11.8

12

33.0

32.5

60,000

10

32.0

8

30.8

40,000

31.0

30.4

6

4

30.0

20,000

3.7

2

29.0

-

0

28.0

FY14

FY15

FY16

FY17E

FY18E

FY14

FY15

FY16

FY17E

FY18E

Deposits

Growth (%)

Source: Company, Angel Research

Source: Company, Angel Research

December 1, 2016

3

Federal Bank | Company Update

Asset quality stress has started stabilizing

Slippages had been relatively higher for Federal Bank for all the quarters in FY16.

However in 1Q and 2Q of FY17, the bank delivered meaningful control over

slippages and this was an encouraging sign. In absolute terms, the slippages were

`280cr and `266cr vs. `571cr in Q3FY16 and `536cr in Q4FY16. While it’s too

early to say that the trouble is over, the initial sign has been clear and that is

incrementally there could be lower slippages.

While it is difficult to quantify the impact of demonetization on the industry, SME

segment do have large exposure to the cash form of business either for input or for

the finished goods that they deal with. However, it is safe to assume some

incremental stress on the SME.

Exhibit 6: GNPAs & NNPAs Ratio yearly trend

Exhibit 7: GNPAs & NNPAs Ratio quarterly trend

3.00

2.84

3.5

2.70

2.73

3.1

2.9

2.8

2.9

3.0

2.8

2.50

2.6

2.15

2.04

2.5

2.00

1.64

2.0

1.49

1.7

1.6

1.7

1.6

1.50

1.3

1.5

1.10

1.0

1.00

0.74

0.73

1.0

0.50

0.5

-

0.00

Q1FY16

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

FY14

FY15

FY16

FY17E

FY18E

GNPAs %

NNPAs %

GNPAs (%) NNPAs (%)

Source: Company, Angel Research;

Source: Company, Angel Research

Credit cost remained elevated for FY16; however, we have started witnessing some

moderation in the same. Accordingly, we expect credit cost top fall to 110bps in

FY17 and further to 80bps in FY18. The bank might take higher provisions in

order to improve its PCR. However, on a like to like basis we don’t expect sharp

rise in provisioning.

Exhibit 8: Credit Cost (%)

Exhibit 9: PCR (%)

1.4

90.0

83.4

84.7

1.2

80.0

72.2

1.2

1.1

70.4

70.0

64.7

1.0

0.8

60.0

0.7

0.8

50.0

0.6

40.0

30.0

0.4

0.2

20.0

0.2

10.0

0.0

0.0

FY14

FY15

FY16

FY17E

FY18E

FY14

FY15

FY16

FY17E

FY18E

Source: Company, Angel Research

Source: Company, Angel Research

December 1, 2016

4

Federal Bank | Company Update

Slippages from SME could see some stress post demonetization,

but improvement in corporate book gives comfort

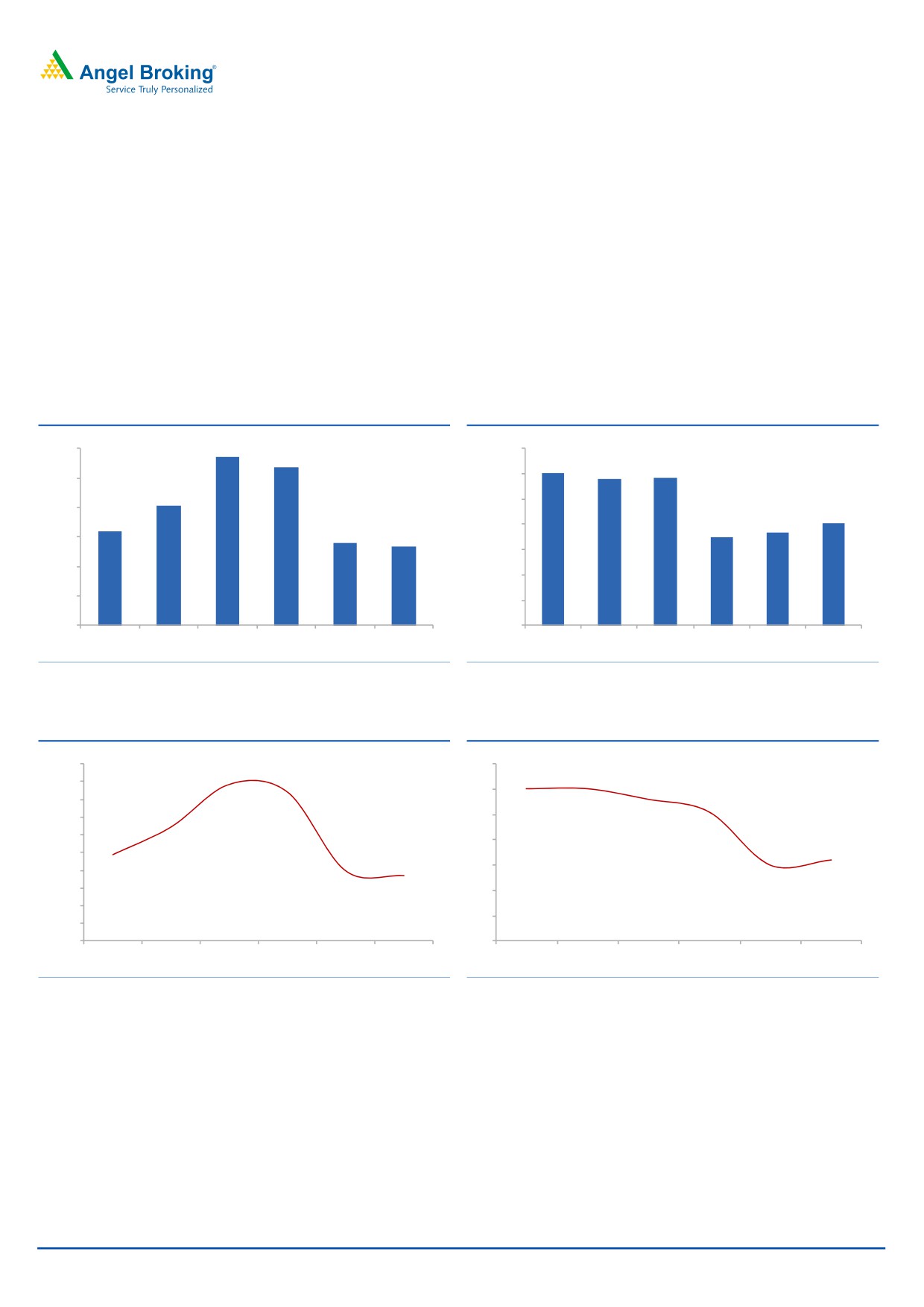

Federal Bank’s pipeline of accounts with potential stress was relatively lower and

was one of the lowest in recent quarters, when they declared their Q2FY17 results.

The expected slowdown in the economy post demonetization could put some

pressure on the SME loan book. However, we don’t expect material deterioration

in the corporate loan book segment for the bank. While in Q2FY17, the bank

witnessed some incremental restructuring, we don’t expect large accounts to come

forward for restructuring in the near term. Further there are a couple of accounts

which should get upgraded from the restructured book in the quarters to come.

Exhibit 10: Slippages (` Cr)

Exhibit 11: Restructured Loan (` Cr)

571

600

3,500

536

3,018

2,889

2,920

3,000

500

405

2,500

400

2,012

317

1,839

2,000

1,755

280

300

266

1,500

200

1,000

100

500

0

-

Q1FY16

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q1FY16

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Source: Company, Angel Research;

Source: Company, Angel Research

Exhibit 12: Slippages Ratio (%)

Exhibit 13: Restructured Loan (%)

7

5.00

4.42

4.20

6.0

6.0

4.50

5.6

6

4.00

5.1

3.22

3.50

5

3.00

2.44

4

3.2

2.50

1.98

3.0

1.85

3

2.00

1.50

2

1.00

1

0.50

0.00

0

Q1FY16

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Q1FY16

Q2FY16

Q3FY16

Q4FY16

Q1FY17

Q2FY17

Source: Company, Angel Research;

Source: Company, Angel Research

December 1, 2016

5

Federal Bank | Company Update

High credit cost dented the return ratios so far, expect RoE to

bounce back in FY18:

Higher slippages dented the RoE both due to reversal of interest and rise in

provisions. However, the lower slippages expected in the coming years, would

normalize the return ratios and we expect RoE to scale back to 10% trajectory by

FY18. Further, accelerated loan growth should also support higher fees income

and consequently RoE

Exhibit 14: Cost/ Income (%)

Exhibit 15: NIM Trend (%)

58

56.7

3.1

3.1

56

3.1

3.0

53.5

52.9

54

3.0

3.0

3.0

52

50.0

3.0

50

47.6

2.9

2.9

48

2.9

46

44

2.8

42

2.8

FY14

FY15

FY16

FY17E

FY18E

FY14

FY15

FY16

FY17E

FY18E

Source: Company, Angel Research;

Source: Company, Angel Research

Exhibit 16: ROA (%)

Exhibit 17: ROE (%)

1.4

1.3

14.0

13.0

12.1

1.2

1.2

12.0

10.1

1.0

10.0

0.9

8.5

0.8

0.8

8.0

5.9

0.5

0.6

6.0

0.4

4.0

0.2

2.0

0.0

0.0

FY14

FY15

FY16

FY17E

FY18E

FY14

FY15

FY16

FY17E

FY18E

Source: Company, Angel Research;

Source: Company, Angel Research

December 1, 2016

6

Federal Bank | Company Update

Outlook and valuation

Federal Bank has already recognized large part of the troubled assets as NPAs.

While there could be incrementally some degree of stress on the SME book, we

believe gradually there should be overall improvement in the asset quality, backed

by corporate loan book. Post Q1FY17 results, when the outlook changed towards

asset quality, the stock appreciated sharply; but subsequently has corrected amid

concerns over slowdown and stress on the SME book. At the CMP, the stock is

trading at 1.4x it FY18 Adj BV. We upgrade the stock to BUY with a target price of

`85.

December 1, 2016

7

Federal Bank | Company Update

Income statement (Standalone)

Y/E March (` cr)

FY14

FY15

FY16

FY17E

FY18E

Net Interest Income

2,229

2,380

2,504

2,899

3,292

- YoY Growth (%)

12.9

6.8

5.2

15.8

13.6

Other Income

694

878

786

1,030

1,107

- YoY Growth (%)

4.4

26.6

(10.5)

31.0

7.5

Operating Income

2,922

3,259

3,291

3,929

4,399

- YoY Growth (%)

10.7

11.5

1.0

19.4

12.0

Operating Expenses

1,392

1,631

1,867

2,079

2,352

- YoY Growth (%)

18.0

17.2

14.5

11.4

13.1

Pre - Provision Profit

1,530

1,628

1,424

1,849

2,047

- YoY Growth (%)

4.9

6.4

(12.5)

29.9

10.7

Prov. & Cont.

318

107

704

739

679

- YoY Growth (%)

19.8

(66.5)

559.6

4.9

(8.1)

Profit Before Tax

1,212

1,521

720

1,111

1,368

- YoY Growth (%)

1.5

25.5

(52.7)

54.3

23.2

Prov. for Taxation

373

515

244

365

410

- as a % of PBT

4.9

38.1

(52.6)

49.5

12.5

PAT

839

1,006

476

746

958

- YoY Growth (%)

0.1

19.9

(52.7)

56.8

28.4

Balance sheet (Standalone)

Y/E March (` cr)

FY14

FY15

FY16

FY17E

FY18E

Share Capital

171

171

344

344

344

Reserve & Surplus

6,780

7,567

7,747

8,405

9,123

Net Worth

6,951

7,738

8,091

8,749

9,467

Deposits

59,731

70,825

79,172

89,777

1,03,987

- Growth (%)

3.7

18.6

11.8

13.4

15.8

Borrowings

5,688

2,308

2,177

1,796

3,120

Other Liab. & Prov.

2,224

1,979

1,991

2,461

2,164

Total Liabilities

74,594

82,850

91,430

1,02,782

1,18,738

Cash Balances

3,104

3,380

3,775

4,040

4,679

Bank Balances

1,425

1,400

1,645

1,796

2,080

Investments

24,118

20,569

22,217

23,342

25,997

Advances

43,436

51,285

58,090

68,600

80,253

- Growth (%)

(1)

18

13

18

17

Fixed Assets

425

467

520

515

530

Other Assets

2,086

5,750

5,183

4,489

5,199

Total Assets

74,594

82,850

91,430

1,02,782

1,18,738

- Growth (%)

5.0

11.1

10.4

12.4

15.5

December 1, 2016

8

Federal Bank | Company Update

Ratio analysis (Standalone)

Y/E March

FY14

FY15

FY16

FY17E

FY18E

Profitability ratios (%)

NIMs

3.1

3.0

2.9

3.0

3.0

Cost to Income Ratio

47.6

50.0

56.7

52.9

53.5

RoA

1.2

1.3

0.5

0.8

0.9

RoE

12.1

13.0

5.9

8.5

10.1

B/S ratios (%)

CASA Ratio

30.8

30.4

32.5

34.0

35.0

Credit/Deposit Ratio

72.7

72.4

73.4

76.4

77.2

CAR

15.3

15.5

13.9

13.2

12.4

- Tier I

14.6

14.8

13.4

12.7

11.9

Asset Quality (%)

Gross NPAs

2.70

2.04

2.84

2.73

2.15

Net NPAs

0.74

0.73

1.64

1.49

1.10

Slippages

1.14

1.82

3.62

2.07

1.55

Loan Loss Prov. /Avg. Assets

0.7

0.2

1.2

1.1

0.8

Provision Coverage

83.4

84.7

72.2

70.4

64.7

Per Share Data (`)

EPS

9.8

11.7

2.8

4.3

5.6

BVPS

81.3

90.3

47.1

50.9

55.1

ABVPS

77.5

86.0

41.5

45.2

49.9

DPS

1.0

1.1

0.7

1.1

1.3

Valuation Ratios

PER (x)

7.1

6.0

25.3

16.1

12.6

P/ABVPS (x)

0.9

0.8

1.7

1.5

1.4

Dividend Yield

1.4

1.6

1.0

1.6

1.9

DuPont Analysis

Interest Income

9.5

9.4

8.9

8.5

8.1

Interest Expenses

6.5

6.4

6.0

5.5

5.1

NII

3.1

3.0

2.9

3.0

3.0

Non Interest Income

1.0

1.1

0.9

1.1

1.0

Total Revenues

4.0

4.1

3.8

4.0

4.0

Operating Cost

1.9

2.1

2.1

2.1

2.1

PPP

2.1

2.1

1.6

1.9

1.8

Total Provisions

0.4

0.1

0.8

0.8

0.6

PreTax Profit

1.7

1.9

0.8

1.1

1.2

Tax

0.5

0.7

0.3

0.4

0.4

ROA

1.2

1.3

0.5

0.8

0.9

Leverage

10.5

10.2

10.8

11.1

11.7

RoE (%)

12.1

13.0

5.9

8.5

10.1

December 1, 2016

9

Federal Bank | Company Update

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.

Disclosure of Interest Statement

Fedral Bank

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

December 1, 2016

10